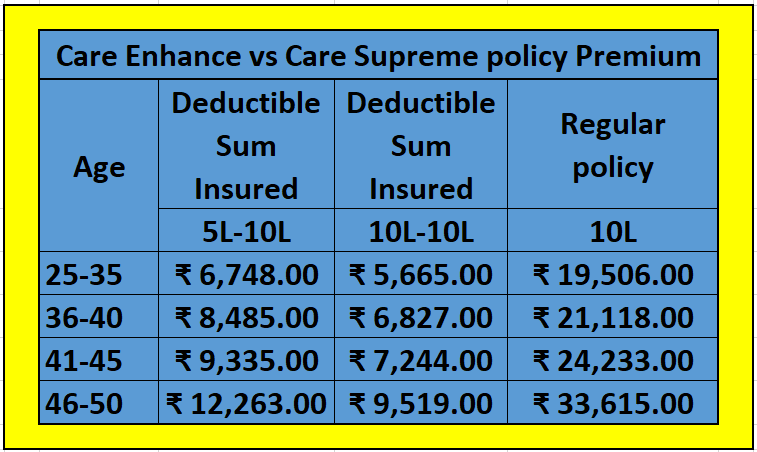

Health Insurance Top up Plan

*What is a Top-Up Policy?*

A Top-Up policy is an additional health insurance plan that provides extra coverage on top of an existing primary insurance policy (for example, corporate insurance). It is primarily used by employees of companies, as they already have health insurance provided by their company and may need additional coverage.

*How does a Top-Up Policy work?*

For example, if you are working in a corporate company and have a health insurance policy of ₹5 lakh or ₹10 lakh, the initial ₹5 lakh or ₹10 lakh is covered by your primary policy. However, if your hospital expenses exceed this amount, a Top-Up policy comes into play.

*Key Features of a Top-Up Policy:*

- *Deductible:* A Top-Up policy has a "deductible" concept, which means that you must first pay a certain amount (your deductible) before the Top-Up policy starts covering the expenses. For instance, with a ₹5 lakh deductible, you will have to bear the first ₹5 lakh of expenses, and any hospital bills beyond this will be covered by the Top-Up policy.

- *Cover Limit:* After your primary policy limit is exhausted, the Top-Up policy will cover the remaining expenses. For example, if you have a ₹10 lakh insurance policy, the first ₹5 lakh or ₹10 lakh is covered by your corporate policy. Any additional bills will be covered by the Top-Up policy.

*Who benefits from a Top-Up Policy?*

- *Corporate Employees:* Many corporate employees already have a health insurance policy provided by their company. However, they may choose a Top-Up policy to upgrade their coverage. This helps in covering expenses that exceed the limits of their corporate policy.

- *After Retirement or Job Change:* When you leave your job, you may lose your corporate health insurance coverage. In such cases, you can convert the Top-Up policy into a regular health insurance policy, ensuring continuous coverage.

*Benefits of a Top-Up Policy:*

- *Lower Premiums:* A Top-Up policy allows you to get more coverage at a much lower premium compared to a regular health insurance policy.

- *Additional Coverage:* You can obtain extra coverage after using up your corporate policy’s limit.

- *Can Be Converted into a Regular Policy:* After retirement or job change, you can convert your Top-Up policy into a regular health insurance policy, ensuring that you remain covered even if you face any major health issues in the future.

In summary, a Top-Up policy provides an affordable way to increase your health insurance coverage, especially when your existing policy limits are exhausted, and it can also be converted into a regular policy after you leave your job or retire.