Advantage of Long Term Home Loan

How a Home Loan Strategy Could Help You Build Wealth: A Smart Approach to EMI and SIP

Taking a home loan is one of the biggest financial commitments in life. But what if you could use that commitment as an opportunity to not only pay off your loan faster, but also build wealth along the way? Here's an interesting strategy that shows how adjusting your home loan tenure and investing the difference in monthly EMIs into a high-return mutual fund can accelerate your loan repayment and potentially create substantial wealth over time.

The Home Loan Dilemma: 20 Years vs. 30 Years

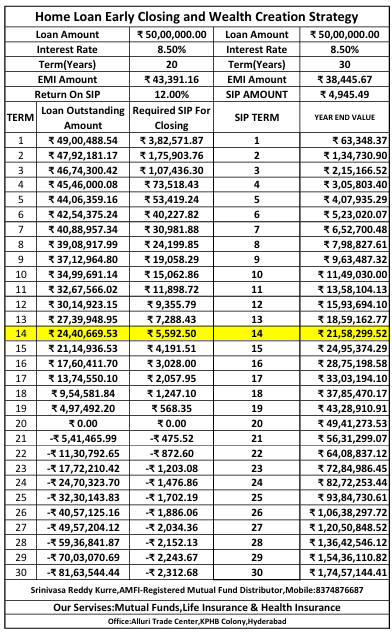

Let’s break it down with an example. Suppose you take a home loan of ₹50 lakh at an interest rate of 8.5%. The EMI for a 20-year loan would be ₹43,391 per month, while for a 30-year loan, the EMI reduces to ₹38,445.

On the surface, the longer tenure (30 years) seems like a disadvantage, because the total interest paid over 30 years is higher than the interest paid on a 20-year loan. However, here's where the strategy becomes interesting: the difference in EMI between the 20-year and 30-year loan is ₹4,946 per month.

The Secret to Building Wealth: SIPs with the EMI Difference

Instead of just paying the lower EMI for 30 years, imagine you invested the ₹4,946 monthly (the difference between the two EMIs) into a Systematic Investment Plan (SIP) in a mutual fund that generates a return of around 12% annually.

By doing so, you could pay off your home loan in just 14 years, rather than 30 years. The compounding effect of the SIP combined with disciplined investing could significantly shorten your loan tenure.

Even more exciting is the long-term potential of this strategy. If you continue both your home loan EMI (of ₹38,445) and SIP (of ₹4,946) for the full 30 years, you could accumulate an impressive ₹1.74 crore—along with the ownership of your home. The SIP would act as an additional investment vehicle that helps you grow wealth, all while reducing the burden of your loan repayment.

Why Does This Work?

The key to making this strategy successful lies in two factors: time and disciplined investing. By investing the EMI difference into a high-return instrument like mutual funds, you take advantage of compounding returns. Over time, the wealth generated through the SIP can not only help you pay off your loan faster but also provide you with a significant amount of savings.

A Word of Caution

While this strategy may sound enticing, it’s important to understand that it requires strict financial discipline. Implementing this strategy successfully means being committed to both the SIP and the loan repayments. Missing either the SIP contribution or the EMI could derail the entire plan.

Excel sheets and financial calculators are great tools for planning, but the real challenge lies in consistent execution. This approach is best suited for individuals who can manage their finances with discipline, sticking to their goals and ensuring that both the EMI and SIP payments are made regularly.

In Conclusion

The long-term impact of combining home loan EMI payments with a disciplined investment strategy can be incredibly powerful. Not only can it help you pay off your home loan faster, but it can also allow you to build substantial wealth over time. If you're considering a home loan, think beyond just the EMI and explore how you can use the difference to invest in your future.

Remember, it's not just about the numbers on an Excel sheet—it’s about the commitment to your financial goals and your ability to execute a well-thought-out strategy. With the right mindset and financial discipline, you can not only own your home but also create a substantial financial cushion for the future.